Social Security, The Chance to Make a Huge Mistake

Think of Social Security as an asset to be managed. It may be a bit of an abstract thought since it is impossible to call up Social Security and ask for a withdrawal. Still, the lifetime value of your Social Security benefit is likely to be substantial, and can be dramatically larger or smaller depending on your claiming strategy, timing, and longevity.

In my role as a financial planner, I interact with people at various stages of life. If I were to categorize these stages in retirement planning terms, in very rough terms, there are four: pre-accumulation, accumulation, transition, and retirement. Each stage is important and has certain common features and needs, but the mistakes that we see tend to be concentrated in the transition years.

We’ve often referred to the transition years as the Retirement Red Zone, in a reference to the NFL Red Zone, the last 20 yards to the goal line. There’s extra pressure and anxiety, just like in the NFL. We typically can sense that anxiety in clients around 5-7 years before retiring from full time employment, and it often extends into the first year or two of retirement. And why would that be? There are a number of anxiety factors outside of money, including change of social network and purpose, but money always plays a major role. The major source of income is soon going to be shut off, and how will you comfortably and reliably fill that gap?

There is a lot going on, and clients often feel that something has to be done. A solid Retirement Income plan should consider pensions, portfolio positioning in extreme detail, reliability of expected returns, liquidity, order of asset use, tax planning, part-time employment, inheritance, gift planning, and of course, Social Security.

I tend to think about Social Security as an asset to be managed. I am not sure that other people do, however, since it is impossible to call up Social Security and ask for a withdrawal. Still, the lifetime value of your Social Security benefit is likely to be substantial, and can be dramatically larger or smaller depending on your claiming strategy, timing, and longevity.

There is one misunderstanding that comes up frequently. Clients and Prospective clients often indicate that they intend to quickly fill the lack of employment income with Social Security. I suspect that it feels better emotionally to have the money coming in. Digging deeper, some clients have mentally combined their desired retirement date with their intention of when to claim Social Security, as a single point in time.

However, after we do our planning work, very few of our financial plans show claiming Social Security early as the best result. It is quite common for the optimal claiming strategy for a married couple will show $300,000 or more in additional projected lifetime benefits over and above the worst claiming strategy. More often than not, claiming at age 62 is the worst strategy available. Yet, for Americans as a whole, age 62 is the most popular filing age. Interestingly, since the 1980’s, about 2/3rds of the population has claimed social security before their FRA, with about half claiming it as soon as possible. https://www.ssa.gov/policy/docs/ssb/v74n4/v74n4p21-text.html#chart1

In real dollar terms for a person in their early 50’s, if your Social Security benefit was $3,000 per month at a Full Retirement Age of 67, you could choose to take your benefit at 62 for about $2,100, or wait until age 70 and receive $3,720, or some number and age in between. Roughly speaking, the benefit has a guaranteed increase of 5-8% per year, plus cost of living adjustments. https://www.ssa.gov/policy/docs/ssb/v74n4/v74n4p21.html

For many clients, we encourage preserving and growing the Social Security benefit for a later date, while using other assets to cover retirement spending in the meantime. I want to be very clear that this general statement is not a prescription for you, as differences in family longevity, health, spouse ages and incomes, prior marriages and deaths, and other factors can all affect your projected benefits, as well as your overall retirement income plan. We go through a lot of discussions, planning, and projections before making a recommendation to any client. Still, the truth is that in our current low interest rate environment, it is rare to find another investment that has a guaranteed increase of 5-8% per year plus a cost of living adjustment.

If you follow this thought to its logical conclusion, for a client to delay claiming Social Security, they have to live on something else for several years, and that can feel uncomfortable. If you are like most, the short story is that you may need 3-8 years or so of providing for your own expenses, during the first, best, and often most expensive retirement years. Let’s face it, you are likely to travel and consume much more entertainment in your 50’s and 60’s than your 80’s or 90’s. Unless you have a pension, generally you have to live mostly off your investments. Of course, it might be fun to pick up part-time work as a supplement, often as a “near-hobby.” Like gardening? Work at the flower shop or garden center. Like guns? Work at the shooting range.

Living nearly completely from a portfolio for a few years often requires uncomfortably high portfolio withdrawal rates. It is not uncommon to be withdrawing 7%, 8%, and sometimes more, per year for a few years. This situation would be completely unsustainable were it not for the relief when Social Security is switched on, at the higher monthly amount. When planned correctly, the Social Security benefit replaces most of the withdrawals and reduces the strain on the portfolio, so that the withdrawal rate is often below 3%, sometimes below 1% after Social Security is on. It is not unusual for a financial plan to show dwindling assets up to the age at which we turn on Social Security, and accumulating assets afterward.

One caveat is that Social Security benefits may change over the next few years, as Congress addresses the financial reality of the future of the program. We’ve addressed that in the past, and regardless of what happens, the benefit will still be significant enough to think carefully about.

There are several other important details to get right during the transition years, and every detail is interwoven with the next. Today I have touched on Social Security, and the importance of getting it right as one element of prudent retirement income planning. As a quick reminder, a solid plan should consider portfolio positioning (in much greater detail than most advisors provide), reliability of expected returns, liquidity, order of use relative to tax planning, inheritance and gift planning, all coordinated with Social Security. That’s what we do well. If you want to chat about it, feel free to call or email me: patrick@maccofinancial.com.

Please note, changes in tax laws may occur at any time and could have a substantial impact upon each person's situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. Keep in mind that there is no assurance that any strategy will ultimately be successful or profitable nor protect against a loss. Investors should consider their personal investment horizon and income tax brackets, both current and anticipated, when making an investment decision, as these may further impact the results of the comparisons. Keep in mind that results will vary as investing involves risk, fluctuating returns, and the possibility of loss. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Patrick Stoa and not necessarily those of Raymond James. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

The Importance of Proper Income Tax Withholding

Would you rather have a dollar today or a dollar tomorrow? What about one dollar every month or twelve dollars at the end of the year? The majority of us would take the money as soon as possible. This is based on two old economic principles; opportunity cost and the time value of money. We know that having a dollar today rather than some time in the future is more valuable because it means we can use that dollar immediately. This could mean saving, paying off debt, or even investing it for the future. Therefore, as we evaluate something of equal value received in the future, we discount its worth and prefer that same value now. This is relevant to us as taxpayers as every month we are given the option to receive more now or more when we file our taxes (assuming we are withholding too much).

Would you rather have a dollar today or a dollar tomorrow? What about one dollar every month or twelve dollars at the end of the year? The majority of us would take the money as soon as possible. This is based on two old economic principles; opportunity cost and the time value of money. We know that having a dollar today rather than some time in the future is more valuable because it means we can use that dollar immediately. This could mean saving, paying off debt, or even investing it for the future. Therefore, as we evaluate something of equal value received in the future, we discount its worth and prefer that same value now. This is relevant to us as taxpayers as every month we are given the option to receive more now or more when we file our taxes (assuming we are withholding too much). And while its obvious to us to take the dollar today versus tomorrow, a 2011 study found that the average federal refund in the state of Wisconsin was $2,462.89. We are no longer talking about a dollar every month but rather $205! That’s a meaningful difference and one that we should not quickly ignore. Sizable tax refunds can be used for good things like paying off debt or saving. But more often than not they are used for less noble options, despite our best intentions. What then can we do to remedy the situation and get funds back in our monthly budget?

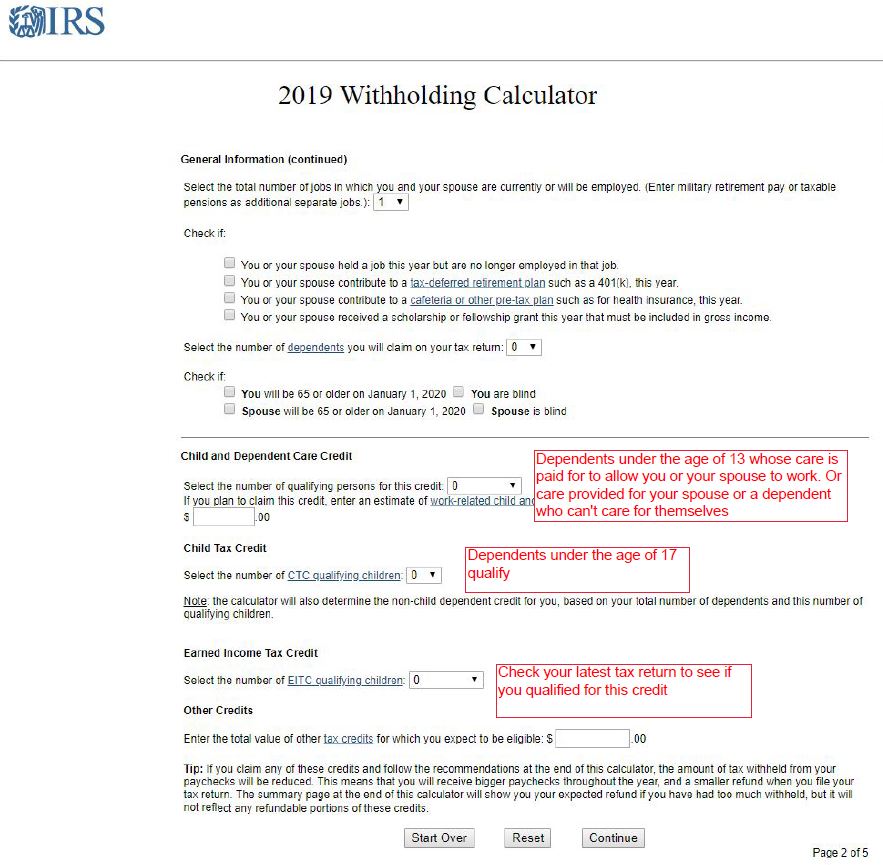

There are a couple of ways to make sure your withholding is as accurate as it can be. The first step is to visit the IRS’s Withholding Calculator. You will need annual income figures, a copy of a your most recent pay stub(s), how much in taxes you have paid so far in the given tax year, and your portion of employer sponsored plan contributions (401(k) 403(b) etc..). The calculator works best if your situation is relatively simple, one or two incomes along with only a few dependents. However, if your situation is more detailed than that, you can still get a good reading from the calculator but having all the relevant figures will be even more important. See the screenshots for more tips when filling out the calculator.

Once you have completed the calculator, you will have a good reading of where you stand for the given tax year. The next task is to complete the IRS’s W-4 worksheet. This is a somewhat duplicative job, but it is also a good proof of your work as it should result in the same recommended allowances as the calculator. If you have a dual income household, make sure you also complete the two earners worksheet on page 4. The end result of completing the W-4 and withholding calculator may mean you need to modify you existing allowances. You will need to work with your employer to adjust the number of allowances you claim. This figure comes from page 1 of the W-4 (see W-4 screenshot below). Some employers may require you to sign and submit this completed W-4 while others are able to make the change without it.

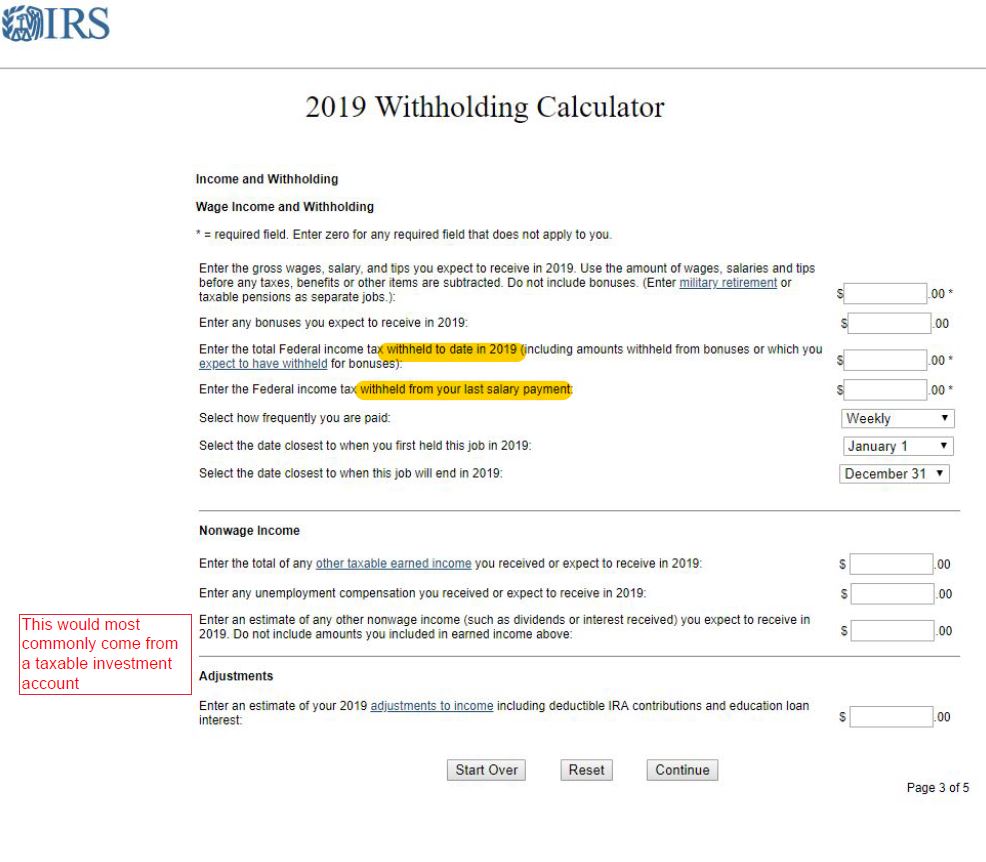

After you have worked with your employer to update your allowances, it’s important to allow 1 or 2 paychecks to flow through the updated withholding. This will produce new figures for how much is taken out of each paycheck for taxes. With these new figures in hand review your work once again. This can be done by redoing the withholding calculator based on the amounts withheld from your latest paycheck and the new amount withheld year to date (see withholding calculator page 3). You can also check your work by extrapolating one month’s withholding into twelve and checking the final figure with your previous year’s taxes paid (make sure to take into account any increase or decrease in earnings as well as fluctuations in pay from month to month, if your compensation is not level). Based on the results of this final check, you can either revise your allowances by repeating the prior steps or continue to withhold at the new amount, if the numbers are correct. By knowing these numbers, you will have a better feel for how your taxes will shake out for the following year. Tax withholding is not an exact science and everyone’s situation is unique. This may mean having to dreadfully “pay in”. But if you can see it coming, hopefully you will be more prepared.

So why go through all of the work if you are going to get the money at the end of the year anyway? I alluded to this point in the opening paragraph. Monthly cash flow is the basis upon which most of us budget and how we direct normal spending. To have the most effective and efficient budget, we need to correctly account for tax withholding. Let’s use the above-mentioned average as an example. If we received $205/mo. and applied that to debt reduction (assuming a $10,000 balance, interest rate of 5%, and a 5-year period) we would be able to pay the loan off almost 6 months earlier when compared to using the same dollar amount but only once per year. And while it’s also true that you are making an “interest free loan to the government” by over withholding, proper tax withholding is less about them and more about you. “With great power comes great responsibility”. Adding these funds back into your monthly budget will mean that every month you will need to be disciplined to make sure that money goes towards its intended purpose.

If you think that this is just too much work, the good news is the IRS has done some of this work for you. A couple articles have run in the last few weeks reporting that Americans are receiving smaller refunds for 2018 compared to previous years. Here is an example from CNBC “Here’s why the average tax refund check is down 16% from last year”. As the article points out, this had been due in part to the fact that Americans are receiving more in wages on a monthly basis and less at the end of the year from a tax refund. This is good news for all of us! It means the IRS has already done a better job of estimating our taxes based on the tax law changes enacted in 2017. While this is a good start, I would still encourage you to look at your own withholding and do the work to see if any changes need to be made.

Andrew Froelich

Financial Advisor

https://www.governing.com/gov-data/finance/average-irs-tax-refund.html

https://www.cnbc.com/2019/02/22/heres-why-your-tax-refund-could-be-smaller-than-last-year.html

While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. Any examples are hypothetical and for illustration purposes only. Actual results will vary.