Why Health Savings Accounts (HSA's) are so Important

A little bit of planning can go a long way in avoiding taxes and having real world results when paying for medical expenses. Recently I experienced this after needing a significant amount of dental work that insurance wouldn’t cover. After diving deeper into Health Savings Accounts and utilizing some of these tax-saving strategies myself, I wanted to share this information.

Unless you are a CPA, financial planner, or tax nerd you probably don’t jump for joy when you think about taxes. Furthermore, almost no one likes having to plan for medical expenses. But a little bit of planning can go a long way in avoiding taxes and having real world results when paying for medical expenses. Recently I experienced this after needing a significant amount of dental work that insurance wouldn’t cover. After diving deeper into Health Savings Accounts and utilizing some of these tax-saving strategies myself, I wanted to share this information.

When it comes to tax advantaged saving, HSA’s are not always top of mind. 401(k)’s, Traditional IRA’s, and Roth IRA’s tend to draw more attention. I think this is a shame as HSA’s are what we like to call tax unicorns. The reason for this is additions to HSA account receive a federal tax deduction, grow tax free, and can be withdrawn tax free as long as the funds are used for qualified medical expenses. It’s almost too good to be true, never paying taxes on money that most Americans anticipate having to spend every year for medical expenses.

In addition to the tax benefits, employers sometimes match contributions to an HSA (up to certain dollar amount per year). In some instances, they will contribute a certain dollar amount regardless of your contributions as long as you are eligible and have an HSA opened. This is a great opportunity to get “free money” an employer is offering.

It’s important to note that HSA’s are similar to other tax advantaged accounts in that their annual contribution is limited and is perishable. Once you have filed your taxes for a given tax year, you can no longer make contributions to your HSA for that year. This indicates that whenever possible, we want to contribute to, or at least funnel expenses through the HSA. If you contribute more to the HSA compared to your expenses, the balance can be used in future years. This same feature is not available in other plans life Flexible Savings Accounts (FSA’s)2.

Ideally, we should plan on funding HSA’s with payroll deductions because of the tax benefits mentioned early. When HSA contributions are made with payroll deductions, not only do they provide a federal tax deduction, they also are not subject to FICA taxes. Not all HSA plans offer this additional layer of tax savings. However, most HSA’s are structured this way as it is usually the most advantageous for the employer as well3. This contribution method is similar to contributions made to a retirement plan as payments are deducted directly from your check and deposited into the HSA.

Alternatively, you can make contributions to your HSA directly from other sources. While slightly less advantageous, the federal tax deduction benefit is still available. Let’s say you have a $1,000 medical expense, $0 in your HSA, but you have the $1,000 set aside in your savings account. You can contribute that $1,000 to your HSA, pay for the medical expense from the HSA via an issued debit card, or “reimburse” yourself the funds and pay for the medical expense a separate way. The concept is to create the tax deduction by contributing to the HSA, and then documenting that you used the HSA money for a qualified medical expense.

What is the hard dollar benefit for utilizing an HSA in this way? Ultimately it depends on what tax bracket you fall into is for any given year. But for illustrative purposes, let’s assume you are a couple making $115,000 with no other deductions except the standard deduction of $24,400 (in 2019). Your adjusted gross income would place you in the 22% marginal tax bracket. Therefore, a $1,000 deduction would in theory save you $220 in federal income taxes.

For this same hypothetical situation, if a family was able to max fund an HSA for a given year, you would receive a 7,100 deduction2 (2020 annual contribution limit). Using the scenario illustrated above, that would equate to a roughly $1,562 reduction in federal taxes. If those funds were also contributed solely through payroll deductions, an additional $543 in FICA taxes could be avoided. Combine these two taxes savings and you have $2,105 in hard dollar tax savings. Furthermore, tax savings may exist on a state level as well. However, because Health Savings Accounts are a federally mandate program, states can choose to comply with the federal guidelines or make their own rules2.

Most HSA plans also include an investment component once the balance hits a certain dollar amount ($2,000 for example). Once reached, you can begin investing any dollars over the requirement. HSA account plans will often offer an investment lineup similar to a 401(k) that you can choose from. Please Note: investing in an HSA can add a layer of complexity that may be too much to manage at first. It’s always prudent to make these decisions with an additional level of caution. If you anticipate needing the funds within a relatively short time frame, it’s likely best to leave it in cash or use a low risk investment vehicle like a money market mutual fund.

HSA’s do add some extra work when filing your taxes. However, if you work with a CPA, the required forms are common. If you file your own taxes, most major tax prep software has easy to understand modules that help you file your HSA related forms correctly.

Hopefully by you now see why Health Savings Accounts can be so beneficial. You get the best of both worlds when it comes to taxes, it’s a great way to practice saving for medical expenses, and if you are able you can put your money to work through investments. Understandably, there are lots questions that come up when using an HSA that require detailed answers. For the most accurate and up to date information visit: https://www.irs.gov/publications/p969 This page can be daunting as it stores a lot material that may not be relevant to you. However, it offers the best information out there about HSA’s.

Andrew Froelich

CERTIFIED FINANCIAL PLANNER™

Sources:

1 https://www.optumbank.com/all-products/hsa/hsa-eligibility.html

2 https://www.irs.gov/publications/p969

3 https://www.hsaedge.com/2018/09/23/reduce-social-security-and-medicare-taxes-with-an-hsa/

The Importance of Proper Income Tax Withholding

Would you rather have a dollar today or a dollar tomorrow? What about one dollar every month or twelve dollars at the end of the year? The majority of us would take the money as soon as possible. This is based on two old economic principles; opportunity cost and the time value of money. We know that having a dollar today rather than some time in the future is more valuable because it means we can use that dollar immediately. This could mean saving, paying off debt, or even investing it for the future. Therefore, as we evaluate something of equal value received in the future, we discount its worth and prefer that same value now. This is relevant to us as taxpayers as every month we are given the option to receive more now or more when we file our taxes (assuming we are withholding too much).

Would you rather have a dollar today or a dollar tomorrow? What about one dollar every month or twelve dollars at the end of the year? The majority of us would take the money as soon as possible. This is based on two old economic principles; opportunity cost and the time value of money. We know that having a dollar today rather than some time in the future is more valuable because it means we can use that dollar immediately. This could mean saving, paying off debt, or even investing it for the future. Therefore, as we evaluate something of equal value received in the future, we discount its worth and prefer that same value now. This is relevant to us as taxpayers as every month we are given the option to receive more now or more when we file our taxes (assuming we are withholding too much). And while its obvious to us to take the dollar today versus tomorrow, a 2011 study found that the average federal refund in the state of Wisconsin was $2,462.89. We are no longer talking about a dollar every month but rather $205! That’s a meaningful difference and one that we should not quickly ignore. Sizable tax refunds can be used for good things like paying off debt or saving. But more often than not they are used for less noble options, despite our best intentions. What then can we do to remedy the situation and get funds back in our monthly budget?

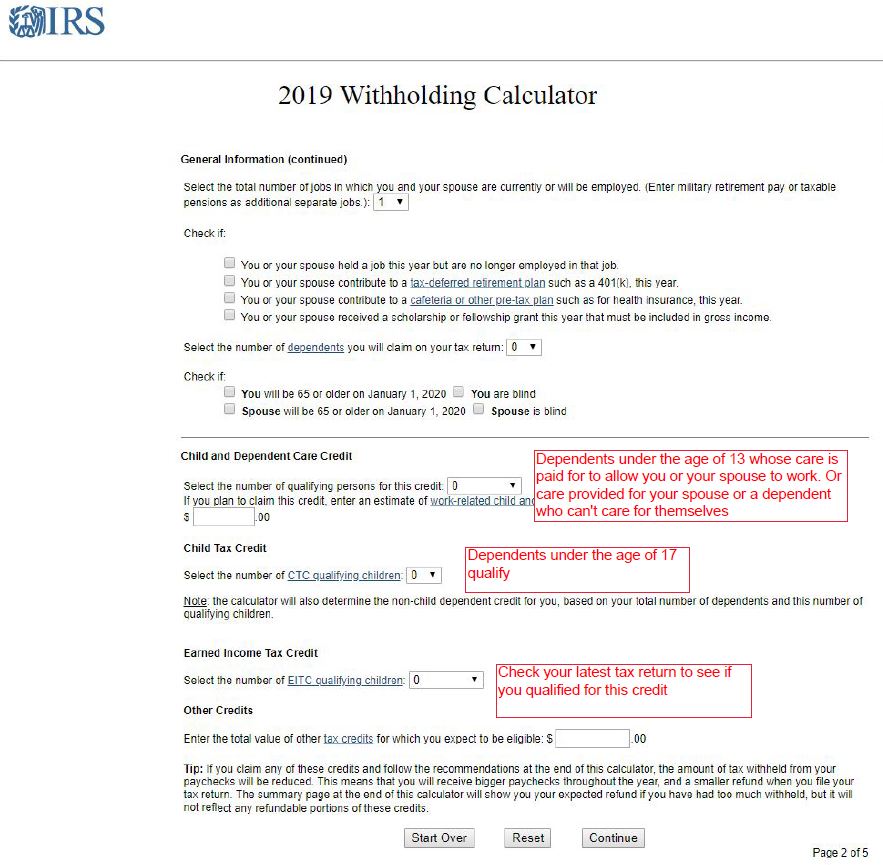

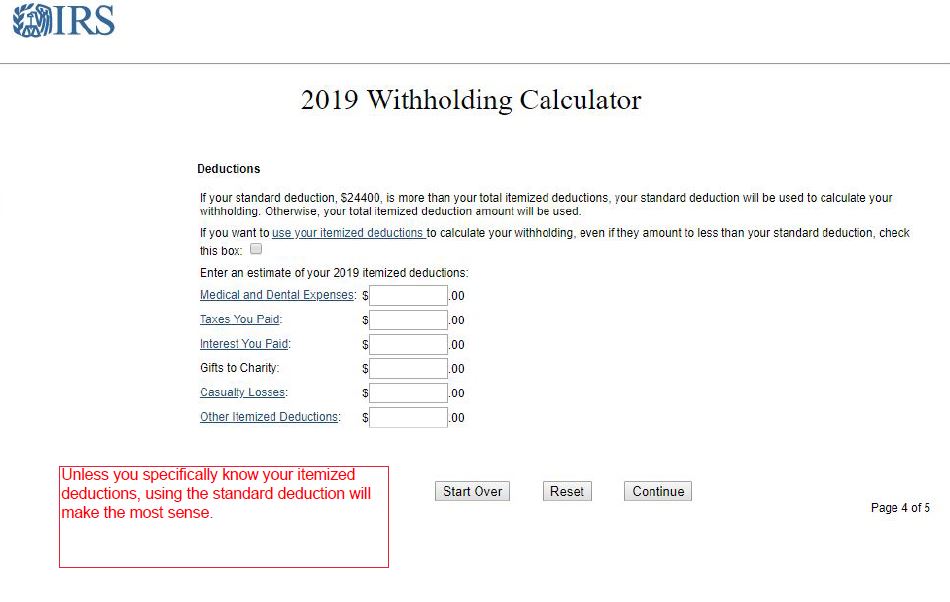

There are a couple of ways to make sure your withholding is as accurate as it can be. The first step is to visit the IRS’s Withholding Calculator. You will need annual income figures, a copy of a your most recent pay stub(s), how much in taxes you have paid so far in the given tax year, and your portion of employer sponsored plan contributions (401(k) 403(b) etc..). The calculator works best if your situation is relatively simple, one or two incomes along with only a few dependents. However, if your situation is more detailed than that, you can still get a good reading from the calculator but having all the relevant figures will be even more important. See the screenshots for more tips when filling out the calculator.

Once you have completed the calculator, you will have a good reading of where you stand for the given tax year. The next task is to complete the IRS’s W-4 worksheet. This is a somewhat duplicative job, but it is also a good proof of your work as it should result in the same recommended allowances as the calculator. If you have a dual income household, make sure you also complete the two earners worksheet on page 4. The end result of completing the W-4 and withholding calculator may mean you need to modify you existing allowances. You will need to work with your employer to adjust the number of allowances you claim. This figure comes from page 1 of the W-4 (see W-4 screenshot below). Some employers may require you to sign and submit this completed W-4 while others are able to make the change without it.

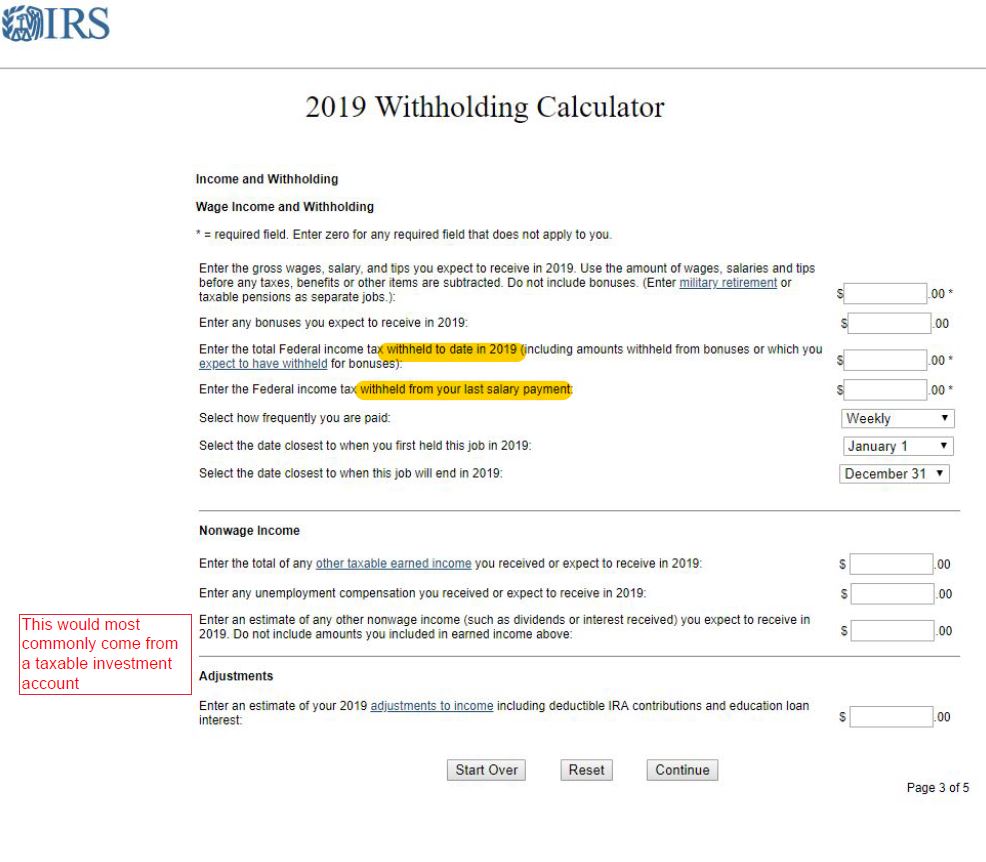

After you have worked with your employer to update your allowances, it’s important to allow 1 or 2 paychecks to flow through the updated withholding. This will produce new figures for how much is taken out of each paycheck for taxes. With these new figures in hand review your work once again. This can be done by redoing the withholding calculator based on the amounts withheld from your latest paycheck and the new amount withheld year to date (see withholding calculator page 3). You can also check your work by extrapolating one month’s withholding into twelve and checking the final figure with your previous year’s taxes paid (make sure to take into account any increase or decrease in earnings as well as fluctuations in pay from month to month, if your compensation is not level). Based on the results of this final check, you can either revise your allowances by repeating the prior steps or continue to withhold at the new amount, if the numbers are correct. By knowing these numbers, you will have a better feel for how your taxes will shake out for the following year. Tax withholding is not an exact science and everyone’s situation is unique. This may mean having to dreadfully “pay in”. But if you can see it coming, hopefully you will be more prepared.

So why go through all of the work if you are going to get the money at the end of the year anyway? I alluded to this point in the opening paragraph. Monthly cash flow is the basis upon which most of us budget and how we direct normal spending. To have the most effective and efficient budget, we need to correctly account for tax withholding. Let’s use the above-mentioned average as an example. If we received $205/mo. and applied that to debt reduction (assuming a $10,000 balance, interest rate of 5%, and a 5-year period) we would be able to pay the loan off almost 6 months earlier when compared to using the same dollar amount but only once per year. And while it’s also true that you are making an “interest free loan to the government” by over withholding, proper tax withholding is less about them and more about you. “With great power comes great responsibility”. Adding these funds back into your monthly budget will mean that every month you will need to be disciplined to make sure that money goes towards its intended purpose.

If you think that this is just too much work, the good news is the IRS has done some of this work for you. A couple articles have run in the last few weeks reporting that Americans are receiving smaller refunds for 2018 compared to previous years. Here is an example from CNBC “Here’s why the average tax refund check is down 16% from last year”. As the article points out, this had been due in part to the fact that Americans are receiving more in wages on a monthly basis and less at the end of the year from a tax refund. This is good news for all of us! It means the IRS has already done a better job of estimating our taxes based on the tax law changes enacted in 2017. While this is a good start, I would still encourage you to look at your own withholding and do the work to see if any changes need to be made.

Andrew Froelich

Financial Advisor

https://www.governing.com/gov-data/finance/average-irs-tax-refund.html

https://www.cnbc.com/2019/02/22/heres-why-your-tax-refund-could-be-smaller-than-last-year.html

While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. Any examples are hypothetical and for illustration purposes only. Actual results will vary.

What does Fiduciary mean, and why does it matter?

Almost all our engagements and recommendations with clients are Fiduciary. Why does that matter to you? Under current regulations, all advisors are now required to act as Fiduciaries for new recommendations in retirement accounts (for example IRA accounts). However, they were not required to do that until very recently, and your account might be grandfathered under the old, weaker, “suitability” rules.

You may have heard the term fiduciary. Perhaps you even have a sense that there is something important about it, but you are not quite clear on exactly what it means or why it is important. Let’s help you with that, starting with a little history.

The story of this word probably started at the dawn of humanity, but we can knowingly document it’s conceptually history back to about 3,800 years ago, with the Code of Hammurabi (Circa 1790 BC). Within the Code, about half of the laws dealt with trade, liability, and care of other’s property. Later, Aristotle gave input in the mid 350 B.C. The concept of Fiduciary was solidified in Roman Law. Cicero (106 B.C. to 43 B.C) was quoted as saying:

“Therefore, legal proceedings for betrayal of a commission are established, involving penalties no less disgraceful than those for theft. I suppose because in cases where we ourselves cannot be present, the vicarious faith of friends is substituted; and he who impairs that confidence attacks the common bulwark of all men and, as far as depends on him, disturbs the bonds of society. For we cannot do everything ourselves; different people are more capable in different matters” (“Oration for Sextus Roscius of America”).

In it’s current form, the word Fiduciary comes from the Latin rood Fiducia, which means “trust, confidence, assurance, and reliance.”

With the very rich and deep history, it is safe to infer that the fiduciary is fundamental to human nature. The word has been put to the test through court cases in many jurisdictions, with predictably similar results. Arguably the current standard in the United States is best represented by the Uniform Prudent Investor Act of 1994. Technically this act is model legislation, and not a uniform law. However, the Uniform Prudent Investor Act or the similar Uniform Trust Code, are widely adopted in several states, and referred to by the courts frequently. In particular, it is instructive to view the Duties that are inherent in the Uniform Prudent Investors Act.

Here we will comment on these duties, but do so with a filter towards the financial advisory business, rather than being a Trustee. The two duties that shine through are:

· Duty of Care (or Standard of Care) - the duty to make reasonable decisions based upon proper due diligence. In plain English, this standard asks the question: “Would a person, of similar responsibility and professionalism, find the recommendations and actions made to be reasonable, given the same available information.” I think it is important to reiterate that this duty requires due diligence. Not asking basic questions about a client’s situation would be a failure of this duty, as would placing clients in strange or concentrated investments without a good reason to do so.

· Duty of Loyalty – the duty to place the client’s interest as primary. If there are conflicts, they must be avoided and/or reduced, and they must be disclosed. If a trustee, or an advisor, recommends something because of their own benefit, that is a conflict. The advisor must attempt to be impartial in their dealings.

There are other named duties in the act, such as to diversify, to control costs, and to monitor, although each of these can be inferred from the Duty of Care.

Almost all our engagements and recommendations with clients are Fiduciary. Why does that matter to you? Ironically, many advisors were not required or did not follow a Fiduciary standard. Under current regulations, all advisors are now required to act as Fiduciaries for new recommendations in retirement accounts (for example IRA accounts). However, they were not required to do that until very recently, and your account might be grandfathered, with some specific exceptions, under the old, weaker, “suitability” rules.

We have seen situations where people have come to us to “fix the mess” from other advisors. In the last year we have seen prospective clients with portfolios that were inappropriate for a variety of reasons, including portfolios that were too aggressive, very illiquid, over-concentrated in certain sectors, or locked up in products with high surrender fees. None of these situations would have passed a fiduciary standard. Unfortunately, they were all sold by someone following the lower suitability standard.

We’d love to implement your financial plan with the diligence and process that a fiduciary standard calls for. If you have any questions, please feel free to reach out to us.

- Patrick Stoa

College Planning: Grants, Work-Study, and Loans

In our prior videos (College Planning), we have talked about ways to reduce the cost of education through AP course, college selection, and scholarships. Assuming you have done that and still have a shortfall, you are probably moving on to methods of obtaining financial aid. Today we are going to talk about the $150 billion in federal aid that the US Department of Education offers to 15 million students each year. The aid is provided in the form of grants, work-study, and loans.

In our prior videos (College Planning), we have talked about ways to reduce the cost of education through AP course, college selection, and scholarships. Assuming you have done that and still have a shortfall, you are probably moving on to methods of obtaining financial aid. Today we are going to talk about the $150 billion in federal aid that the US Department of Education offers to 15 million students each year.

Before getting into it, there is a common form that most students and parents will fill out, called the FAFSA (link), or the Free Application for Financial Student Aid. If you have your tax and investment documents together, the FAFSA form is neither difficult nor time consuming to complete. The FAFSA form calculates something called the Expected Family Contribution (EFC). The EFC is exactly as it sounds: the amount that the parents and child are expected to contribute toward the child’s educational expenses for that year. It is worth noting, that many states including Wisconsin (link), also have aid forms available, that you probably should also fill out to attempt to receive their aid.

Each college you are considering has their own number called the Cost of Attendance (COA). Quite simply, if the COA is higher than the EFC, then you have a reasonable likelihood of receiving some form of financial aid. The aid can be awarded in grants, work-study, or loans.

Grants of course are the most attractive, because they don’t have to be repaid. If some of your aid comes as grants, rejoice! Quite simply, however, there is not enough money to go around to make it free for everyone.

That means we move on to work-study programs. The ideal work-study job is one in which little actual work needs to be done. My favorite example is the parking lot attendant. Perhaps a car leaves every 15 minutes or so, where you need to accept payment, which takes perhaps 30 seconds. Then you have another 10-20 minutes to be reading or studying before the next car comes along. This is an ideal situation – the employer needs someone there, but the work only happens intermittently.

Last, loans. Let me caution you here. Loans dig a deeper hole. As of 2015 here in Wisconsin, for students that take loans, the average loan balance is $29,000 at graduation(1). Nationwide, former students owe $1.26 trillion(2). With that in mind, I want to reiterate how important it is to be sure that the courses and majors you are pursuing are likely to have a reasonable career with an income that can support your student loan repayment, along with your other goals. I am personally aware of someone that spent $200,000 on an undergraduate degree that they are not using and will not use. I don’t know the exact amount that was borrowed, but surely some of it was. That was clearly a poor use of that money, essentially a 4 year expensive vacation from reality.

Take note that some loans are federally subsidized, which at ground level means lower interest rates, payments delayed until you graduate or leave school, and in some careers may mean partial loan forgiveness. Private (non-subsidized) loans, on the other hand, have much less favorable interest rates and payment terms.

To sum it up, be sure to do the FAFSA to take a shot at receiving aid.

Warmly,

Patrick Stoa

Financial Advisor

[1] $29,000 per WI student: http://ticas.org/posd/map-state-data

[2] $1.26 Trillion total: https://www.newyorkfed.org/microeconomics/hhdc(2nd chart with the detail of the Non-Housing Debt Balance, Q1 2016

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

College Planning: Athletic, Academic, Community, Specialty, and Workplace Scholarships

In our first college planning video, we highlighted advanced placement credits, college selection, and military scholarships. Today we are going to talk about other scholarships: athletic, academic, and community/specialty/employer scholarships.

In our first college planning video, we highlighted advanced placement credits, college selection, and military scholarships. Today we are going to talk about other scholarships: athletic, academic, and community/specialty/employer scholarships.

First of all, let’s talk about something that many athletes dream about: The Full Ride. I hate to burst your bubble, but it is not common at all. First of all, Division 3 schools cannot give athletic scholarships. Likewise, Division 1 and 2 schools are typically limited in how many scholarships they can give out per sport. The reality is that they have far fewer to give than they have athletes. So, even if offered, it is quite common for scholarships to be partial scholarships.

Still, if you can get a partial scholarship to do something you like doing, that’s great. Partial scholarships are still great way to cut down on college costs. One of the key things we learned through our daughter pursuing an athletic scholarship is that the coaches want to communicate with the athlete, and not with the parent. The coach and the athlete are the ones that will be practicing together for 4 years, so they have to develop the relationship.

One dilemma: does the school offering the athletic scholarship have the expertise in your desired major(s)? How about your plan B, what if you change your mind partway through and want to go to a different field of study. It happens, a lot. Another thing to consider is that practice and competition schedules are priority number one, so working to supplement your income may be difficult. Social life can be different if your team practices at 6am most days.

Let’s move on to Academic Scholarships. These are great if you can get them. Basically, you are being rewarded for being a good high school student. Typically there is an application of some sort, with grades, test scores, outside activities such as service hours, and an essay taken into account. In some cases, you can submit one application for multiple scholarships. I am mixed about the benefit of a single application for many scholarships. Yes, you easily applied for several, but so did everybody else, and the money is not unlimited. So you are not ahead. Sometimes your school of choice will offer scholarships to applicants who meet certain criteria. For example, at the University of Alabama, high test scores and a high GPA can earn you full tuition even for out of state students. They are not alone in this.

Lastly, let’s talk about Community, Specialty and Workplace scholarships. These can be scholarships that are available to a more limited number of people. Typically to be eligible, you have to live in a certain area, be going into a certain field of study, maybe be in a certain club or activity, or have parents that are employed by a certain company. A well-known example of what I call a specialty scholarship is the Evans Scholar program for golf caddies. As far as workplace scholarships, in our area I am aware of several large employers that give scholarships of $500 to $1,000 a year for children of employees. These are not well advertised, and sometimes you have to actively search for them. The nice thing about these types of scholarships is that far fewer people apply for them, so your odds of being awarded the scholarship go up dramatically.

Best of luck with scholarships. Next time we are going to talk about financial need programs and FAFSA, along with work studies and student loans.

Respectfully,

Patrick Stoa

Financial Advisor.

patrick@maccofinancial.com

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

College Planning: Advance Placement, College Selection, & Military Benefits

Does the potential cost of college have you worried? Today we are going to talk about ways to plan for college costs. There are several ways, but we are going to focus on 3 that I think you can control. This is near and dear to me as I have 6 kids, with the first one just entering her 2nd year of college. Possibly 5 more to go, so I appreciate any avenue to save money while still getting a good value in this area.

Does the potential cost of college have you worried? Today we are going to talk about ways to plan for college costs. There are several ways, but we are going to focus on 3 that I think you can control. This is near and dear to me as I have 6 kids, with the first one just entering her 2nd year of college. Possibly 5 more to go, so I appreciate any avenue to save money while still getting a good value in this area.

Personally, I think the overall strategy for college planning should be one of pursuing a good return on investment for the time and money spent on college. There are really two ways to get a better return on investment – either lower the amount invested, or increase the return. Today we are talking about lowering the amount invested, making it easier to afford to go. We are also going to stick to the things that are almost completely within your control – advanced placement credits, college selection, and military benefits. In a later video we will talk about some things that are nice, like scholarships, but not completely in your control.

Early on, long before a child is selecting a college, you can start to reduce your potential college costs through courses known as Advanced Placement courses your high school may offer. In our case, our local high school offered “AP” courses starting as early as sophomore year. How the basic AP courses work is that the child takes the course at their high school, and at the end of the year they sign up for a test for about $100. If they do well enough on the test, then many colleges will accept that as completed college credits. For example, my oldest daughter left high school with more than a full year of college credits (about 30 credits). The total cost for this was maybe around $1,000. Think about that. That boost allows her to get into higher level courses sooner, and likely get a double major in the same time that others would get a single major. What’s the downside? Not every college accepts the credits. The colleges least likely to accept the credits seem to be the prestigious schools, such as some of the Ivy League schools. However, most of the state schools do allow for AP credits.

Likewise, college selection makes an enormous impact on total cost. The average published tuition cost for local 2 year colleges is about $3,500 a year, compared to around $32,000 for private 4 year colleges. Public Universities are in the middle, around $9,500 for in state students in around $24,000 for out of state students. To help students and their families calculate these costs, many colleges have net cost calculators available on their websites. These calculators will ask a number of questions regarding your situation, let you know of certain scholarships that you may automatically qualify for based on factors such as GPA, SAT or ACT test scores, and analyze your financial situation giving you an estimate of expected aid to help determine what the rough net cost will be. The net calculators are important, since several of the private schools with quite large published tuition rates, will regularly discount to attract good students.

The last of the controllable costs is military benefits. The reason I am including them is that, for the most part, healthy young high school graduates could take advantage of them. And the benefits are quite significant. There are two basic benefits, the first being ROTC, or Reserved Officers Training Corps, and the second being the GI bill. The ROTC program is quite good. It varies by branch, but typically ROTC will pay your full tuition and a small monthly stipend through school at 1,000 or so schools. Some of the branches cover room and board at some colleges too. In exchange, you must serve in the military over the college summers and for a few years. It varies, but 4 years is typical. You also enter the military as an officer. It’s important to note that the military offers this program for medical school as well. The GI bill is used after service when looking to return to school. The benefits are impressive. Generally, if you serve 3 years and have a normal honorable discharge, you typically qualify for these benefits:

• Up to 100% paid tuition (in state), or up to about $21,000 per year at a private school.

• A monthly housing stipend – equal to the military Basic Housing Allowance, which seems to be a minimum of $800 per month, and possibly quite a bit more.

• $1,000 a year for books and supplies.

I bring these military benefits up because they are so impressively good, and so many people could qualify. Next time, we will talk about other scholarships, namely Academic, Athletic, Workplace, and Community and Specialty scholarships.

Respectfully,

Patrick Stoa

Financial Advisor.

patrick@maccofinancial.com

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. Opinions expressed are those of Patrick Stoa and are not necessarily those of RJFS or Raymond James. All opinions are as of this date and are subject to change without notice.

Choosing the Right Investment Manager for Your Needs

Would you like to know how investment managers are selected for your portfolio? It certainly is not a case of “we like this guy,” or “who has the best return.” There is a very clear and defined due diligence process. But because our team of advisors recognize that this many not be visible for you, it seemed valuable to share more about it.

Would you like to know how investment managers are selected for your portfolio? It certainly is not a case of “we like this guy,” or “who has the best return.” There is a very clear and defined due diligence process. But because our team of advisors recognizes that this may not be visible for you, it seemed valuable to share more about it.

Nick Lacy is the Chief Portfolio Strategist for Asset Management Services within Raymond James. Nick took the time to articulate what goes into making investment manager selections. Check out the video, or read more in the blog.

Investment manager selection is step 3 in our 4-Step Investment Process. For a bit of review, step 1 is Forward Looking Capital Market Assumptions based on economic data and indicators. Step 2 is optimizing asset allocation to maximize return potential at various risk levels. For more on the 4 Step process, go to the RJ Freedom Investment Approach page, and click on “The 4-Step Investment Process” tab.

Now back to step 3: manager selection. This is where our advisors want to add top quality managers for each of the appropriate asset classes in the portfolio. By its nature, our due diligence team takes their time, perhaps a year or more, in order to determine if a manager is a fit. We want to understand, how has this manager generated good returns in the past, and can they repeat it in the future? Did they hit a few lucky home runs? Or are they consistent, with a well-designed and consistently executed investment strategy?

In order to determine if a manager is actually consistent, Nick Lacy’s team will ask the manager for 100% of their trading history over the last 5 years, and evaluate every trade. By going into such intense detail, the team can determine what is making the manager successful, and understand what economic environments the manager will perform well or poorly in, going forward. Take note, even great investment managers may not look smart every year, since their process can come in and out of favor compared to the market from time to time. Nick mentions Small-Cap Managers (which are tasked with investing in smaller, lesser known companies), who had a few very poor years, compared to other asset classes. Yet they were doing quite well in early 2016, as Small-Cap investing came back into style, so to speak.

So, when would Nick’s team fire a manager from your portfolios? Normally personnel changes are the catalyst. Because we have done the due diligence, Nick’s team knows who the contributors are on the investment manager’s team. If several of them are exiting, or the leadership is changing, that is a sign to us that things may not continue as we expect. Recently, we made a major change away from a well-known Fixed Income investment manager for just this reason. We don’t want the risk of an unknown team making decisions on your money.

Thank you to Nick and his team for all their time and effort to add a robust process to your investments. If you wish to discuss Investments, feel free to call our office at 920-617-6830.

Respectfully,

Patrick Stoa

Financial Advisor.

patrick@maccofinancial.com

Any opinions are those of Nick Lacy, Mike Macco and Patrick Stoa and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss. Diversification and asset allocation do not ensure a profit or protect against a loss. Keep in mind that there is no assurance that any strategy will ultimately be successful or profitable nor protect against a loss.

Investing is like...Toothpaste.

Are more choices better? The makers of toothpaste certainly think so. But so many choices can lead to indecision and, worse, inaction. Thankfully, people find a way to cut through the noise, buy their toothpaste and, most importantly, actually brush their teeth frequently. Investors could learn from this. Read more about my quirky analogy.

They say, “More choices are better.” I am not so sure. Recently I went to the grocery store to buy toothpaste. Instead of a handful of decent choices, I was assaulted by 122 choices (yes, I counted).

How should I choose between having “Deep Cleaning,” “Optic Whitening,” “Anti-Plaque,” and so many other important sounding features. The selection was overwhelming, and I felt like I knew less about toothpaste than ever. Isn’t that silly? So how does this relate to investments?

Watch our video or read below to find out.

First, did you ever stop using toothpaste due to the confusing choices? Of course not. Like toothpaste, there is an enormous selection of investment possibilities. I have seen some people avoid making a decision about what to invest in due to being so overwhelmed. Sadly, the indecision normally means that money is not invested at all, which works about as well as not using toothpaste.

In the beginning, thankfully, most of us didn’t start out “choosing” a toothpaste. Our parents provided it, and we faithfully stuck it in our mouths. The key was to be brushing with any standard toothpaste to get started early and form the habit. As kids, we weren’t actually good at brushing. But by doing it every day, we got better. And by the time we were adults, it became an automatic habit.

Unfortunately, while most parents indoctrinate their kids into brushing their teeth, few pass along the investment habit. If only they did. The key is the same as brushing: start early, and make it a habit. Don’t let the overwhelming array of investment choices stop you. It is probably best to start with something rather plain anyway. Make the choice to invest. Just start now, and make it a habit. Or better yet, make it automatic.

We are here to help you make it happen.

Cheerfully,

Patrick Stoa

Financial Advisor

920-617-6830

Opinions expressed are those of Patrick Stoa and are not necessarily those of Raymond James. All opinions are as of this date and are subject to change without notice. Investing involves risk, investors may incur a profit or a loss. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Are you financing your past or saving for your future?

It is often argued that there are “good” uses of debt. Yet many people are so burdened by it that they cannot afford to save for the future, which, of course, is not good. In many cases, debt is the hangover from decisions we made months or even years ago…

According to a 2010 National Institute on Retirement Security, the median retirement account balance for Americans aged 55-64 is…wait for it…drumroll please………….. $12,0001. Cue the depressing music. Sad as it may be to quantify this, I’m sure the fact comes as little surprise to many. But why is this? Can some not afford it? Sure. But for many, they just cease to make it a priority. We simply choose to spend our money on other, more immediate things. If that’s you, you may want to check out our recent post & video on cash-flow management. But I think there’s a much larger elephant in the room. Debt.

In researching for this post, I found no shortage of data on debt. Pretty much everyone agrees we (read “Americans”) have a debt problem. As of Q4 2015, the average American debt-carrying household has $15,762 in credit card debt, $27,141 in auto loans, $48,172 in student loans and a $168,614 mortgage.2 With so much debt and the payments that go along with it, it’s no wonder people can’t save for retirement. But we are not without hope! Having counseled hundreds of people through this very issue, I know that a little focus and discipline can go a long way. Let’s do this.

The first thing you need to do if you’re under a pile of debt is to get out from under it. In order to do that, you need to know what you spend and how much money you can commit to accelerating your debt payments. If you need help with that, refer to the link above on cash-flow management. Once you know how much extra money you can throw at your debt. It’s time for the debt snowball! So what’s this debt snowball? I’m glad you asked!

The debt snowball is the process of paying off your debts from smallest to largest. When you pay off one debt, you roll that payment into the next debt and so on and so forth and keep going until you’ve paid off all of your non-mortgage debt. So why do we start with the smallest debt and not the one with the highest interest rate? Because we’re humans and we need little victories. It takes people 18 to 36 months to get through this process. If we don’t see immediate fruits to our labor, many of us will give up. Would you save a little interest if you did it the other way? Maybe. But let’s be honest. If we were such disciplined mathematicians, we wouldn’t be in the situation in the first place would we?

Now if you’ve gone through the hard work of paying off all of your non-mortgage debt, I’m sure you don’t want to all back into it. First up, build a decent emergency fund. I’d say at least $10k. This is your insurance policy and serves to protect you from that unexpected set of tires, transmission, and trips to urgent care. DON’T SKIP THIS STEP! If you start saving for retirement before you have this in place, you’ll be taking a premature distribution at the first sign of trouble. But do it right and you’ll be saving money like a champ and on target for a prosperous retirement.

-Mike Macco

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. Any opinions are those of Michael Macco and Patrick Stoa and not necessarily those of Raymond James. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Want a prosperous retirement? Start with this.

How much money do you need for retirement? How much should you save each month to reach that goal? Can you afford that? What lifestyle can you afford if you save less than that? There is only one way to answer those questions…

How much money do you need for retirement? How much should you save each month to reach that goal? Can you afford that? What lifestyle can you afford if you save less than that? There is only one way to answer those questions. You must know what it takes to live your life now. If you know how much money you need to spend on a monthly basis now, you can work off of that number to determine how much you’ll need per month in retirement. Let me explain. (Warning: a little nerdy math ahead. Stick with it!)

If you think you need $50,000 per year that’s got to come from somewhere. Let’s say you have $18,000/year in social security. So you need to make up a difference of $32,000/year out of your own investments. So how much do you have to have invested to produce that stream of income for 30-40 years of retirement? Of course, that depends on how it’s invested. But generally speaking, we encourage our clients to withdraw only 4-6% of their investments per year. Hopefully growth will replace those withdrawals and over time, your money will last and you’ll be able to leave an inheritance. Withdraw more than that, and not only might you not leave an inheritance, you might run out of money prematurely! So if you wanted to keep your withdrawal rate at say, 5%, you’d need to have $640,000 invested somewhere. ($640,000 *.05 = $32,000). Make sense? But what if you only need $40k per year? Then you’d only need to have $440,000! (($40k-18k)/.05.) And there it is. The power of cash flow management. So how do you do it? It doesn’t have to be like pulling teeth!

At the most basic level, all we need is a monthly number. If you’re like my mother-in-law, (Love you Deb!) you can simply write it all down in a spiral notebook. Or if you use your debit/credit card for everything, just look at a statement. Of course, if you want to get a little nerdier, you can use excel. Or if you want to get REALLY nerdy (Like me. I’m a budgeting junkie.), you can use both excel (My budgeting workbook. Check this out!) and some finance software like Quicken! I’ve also heard good things about YNAB.com (you’re welcome, Alaina) and Mint.com, which is “free” but ad-supported. But no matter what you use, try to record it all. Cash, debit, credit, automatic bill payments, ACH withdrawals, charitable contributions and even salary deferrals. Everything. At this point, you’re probably pretty close to the real answer. Take a victory lap! You’ve done more than most people. You could stop there and be able to do some legitimate long-term planning. But you’ve come so far and you’re nearly done.

Now, when I taught Dave Ramsey’s Financial Peace University class (yes, I’m one of those people), I got in the habit of not only accounting for my monthly spending, but also quarterly spending (Water bill, anyone?), and what I call “eventual spending”. These are expenses that I know I’ll have but I’m not exactly sure when. Like birthday and Christmas gifts, furniture replacement, vacations, home maintenance, car replacement/repair, etc. I just sweep a certain amount into savings each month and let it build up for those eventual expenses. Yes, it’s a lot. But it’s part of your cost of living and you’ll probably spend it in retirement so it needs to be quantified.

Sigh! That’s it. Well, step one. But it’s a huge step. And one that puts you in the driver’s seat. Armed with that budget, a financial advisor like ME is much more able to help YOU figure out what you need and how to get you there. Well done!

-Mike Macco

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Mike Macco, and not necessarily those of Raymond James. Past performance may not be indicative of future results. Investing involves risk and you may incur a profit or loss regardless of strategy selected. The hypothetical investment return figures represented are not intended to reflect the actual performance of any particular security or portfolio. Individual investor's results will vary. Raymond James is not affiliated with and does not endorse Dave Ramsey.

Rebalancing

Imagine a situation where you were at the playground on the seesaw with your older brother. It works well at first. Then winter comes. The next spring you hop on the seesaw again, but it doesn’t work anymore. Your brother grew faster, and now the seesaw is out of balance. He gets on, you fly up on your side, and you’re stuck with your legs dangling in the air, suspended until he lets you down. Your seesaw is out of balance. You need to rebalance to make it work the right way again.

Imagine a situation where you were at the playground on the seesaw with your older brother. It works well at first. Then winter comes. The next spring you hop on the seesaw again, but it doesn’t work anymore. Your brother grew faster, and now the seesaw is out of balance. He gets on, you fly up on your side, and you’re stuck with your legs dangling in the air, suspended until he lets you down. Your seesaw is out of balance. You need to rebalance to make it work the right way again.

In the video, we talk about rebalancing your investment portfolio. Rebalancing is simply one form of investment discipline. Rebalancing implies that something is out of balance, and needs to be returned to its original state. It might go something like this: We meet with a client and discuss their hopes, fears, dreams, and resources. We agree on an appropriate mix of assets to address their situation. We initiate investments to match that asset allocation. Over time, some assets perform better than expected, some about as expected, and some worse than expected. As those realities take place, the asset allocation drifts away from the agreed upon allocation.

Rebalancing is the function of bringing that portfolio back to the originally agreed upon asset mix. This does two things for the client. First, it brings the desired risk/return profile back to where it was intended to be. Second, it adds a discipline to selling off some assets that have risen faster than expected and purchasing assets that have not done so well in order to restore the balance. In simple terms, rebalancing effectively forces the portfolio to sell high priced assets and buy low priced assets.

Of course, there is an issue of frequency. How often should rebalancing take place? In our opinion, it should not be daily, weekly, or monthly. That is generally too short a time-frame for any truly significant shifts to have occurred between asset classes.

Thanks for reading and watching.

Patrick Stoa

For questions, comments, and conversation, call us at 920-617-6830.

The discussion contained in this video is a hypothetical illustration and is not intended to reflect the actual performance of any particular security. Future performance cannot be guaranteed and investment yields will fluctuate with market conditions. Every investor’s situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Re-balancing a non-retirement account could be a taxable event that may increase your tax liability.